About This Newsletter

Welcome to the Collins House Private Wealth client information newsletter, your monthly tax and super update keeping you on top of the issues, news and changes you need to know. Should you require further information on any of the topics covered, please contact us via the details below.

T: 03 9629 6922

E: mail@collinshouse.com

Level 13, 90 Collins Street, Melbourne VIC 3000

PO Box 24175, Melbourne VIC 3000

Collins House Newsletter: December 2023

Give yourself a super gift this Christmas

Give yourself the ultimate gift that doesn’t cost a thing – a super to-do list which is a gift that will benefit you now and in the future.

1. Consolidate your super

With over 10 million unintended multiple superannuation accounts, these multiple accounts are costing Australians an extra $690 million in duplicated administration fees and $1.9 billion in insurance premiums per year, which is eroding many Australians’ hard earned superannuation benefits. If you are one of these individuals with multiple superannuation accounts, there may be benefits to rolling your accounts onto one superannuation fund.

Consolidating your superannuation is now easier than ever, using ATO online services or your myGov account. If you’re not sure whether you might have other superannuation accounts, you can search for lost or unclaimed super via the ATO or by logging into your myGov account linked to the ATO and clicking on Manage my super.

However before you consolidate your funds, there are a few things you should do, such as:

- consider whether you have any insurance cover which may be lost when transferring benefits to a new fund, and

- check on other details such as fees, insurance premiums, variety of investment options available, performance data, and tax implications from consolidating your superannuation to ensure the transfer provides you with better value and meets your needs.

2. Review your investment strategy

Your superannuation fund trustee invests your money for you. Most funds allow you choose from a range of investment options, from conservative to growth. Take the time to check your investment

options and decide what’s right for you. The options you choose can make a big difference to how your super grows between now and your retirement.

If you manage your own self-managed superannuation fund (SMSF), the super laws require you to prepare and implement an investment strategy for your SMSF and review the strategy regularly (ie, at least annually). Your investment strategy is effectively your plan for making, holding and realising assets consistent with your investment objectives and retirement goals.

It also needs to set out why and how you’ve chosen to invest your retirement savings to meet the goals outlined in the strategy. Review your investment strategy to ensure it meets each member’s investment and retirement objectives.

3. Make extra contributions

Making small financial sacrifices and contributing to super over the years is key to long-term wealth. This long-term growth is due to the power of compounding interest. Superannuation uses compounding interest to grow your balance which will help you in retirement. If you’re an employee, your employer will pay 11% of your salary/wages into superannuation in 2023/24 that will benefit from compounding interest and grow until you reach retirement.

To boost the amount you’ll have saved at retirement, you may want to consider making additional contributions through salary sacrificing or making personal after-tax contributions to superannuation. However contribution caps must be considered to avoid exceeding the caps and paying extra tax.

4. Check your insurance

Insurance is another key aspect of your superannuation that you should review. Superannuation funds generally offer three types of insurance for their members, including life insurance, total and permanent disablement (TPD) insurance and income protection insurance, so it’s important to check whether you have any cover within your fund.

Some funds provide a default level of insurance as a standard inclusion when you open your account, but it’s worthwhile seeking advice to determine whether your current level of cover will adequately protect you and your family in the event of injury, illness or death.

5. Check your beneficiary nominations

Despite what many people may think, superannuation is not an estate asset which means on death it does not automatically flow to your estate. This means that your Will does not typically deal with your superannuation benefits.

To make sure your superannuation is distributed to the right people, you should nominate a valid beneficiary. If you don’t nominate a beneficiary or you have an invalid nomination (ie, because your nominated beneficiary does not meet the definition of a superannuation law dependant at the time of your death), your superannuation fund may decide who receives your superannuation money, regardless of what you have in your Will. For this reason, it is important to regularly review your superannuation death benefit nominations* when your circumstances change to ensure it remains up to date and ends up in the hands of the right person(s).

6. Sleigh the super way

Superannuation is your money so it pays to take an active interest in your superannuation during your working years. Reviewing your current superannuation and making these simple changes can help boost the amount you have available for retirement over the long term

Lost or destroyed tax records? Don’t panic!

Now and then, taxpayers may find themselves in a situation where they simply have no records to back up a tax claim. There can be many reasons for this, such as losing documents (either paper or electronic) when moving home, or technology failures that end up with the same result (or worse, destroyed records).

And with a hot summer predicted, let’s not forget the very real danger of natural disasters and the devastation these can have on people’s lives, not just their financial concerns.

It’s true that in these modern times the ATO’s systems are able to pre-fill quite a lot of data, and this is only going to increase over time, which can mean that taxpayers can relax a little more about having to stay on top of record keeping. But there can still be situations where essential back-up documents or other evidence is required that may be unavailable for one reason or another.

If your records are damaged or destroyed or simply missing, there are ways to a remedy, or at least an acceptable outcome. First of all, be assured that we will hold quite a substantial amount of required information, so your first and perhaps best inquiry could be to your friendly tax professional.

But the ATO can also help. It can re-issue or supply copies of tax documents, such as income tax returns, activity statements, or notices of assessment. We can help if you need to request copies of any tax documents.

If you have lost your TFN, we will most likely have that on our records. If for some reason you have not given that to us in the past, it is still possible to interact with the ATO using other information to verify your identity, such as your date of birth, address and bank account details. Your super fund will also have your TFN, but will also require identity verification.

Your employer or payer should have copies of your PAYG payment summaries, and your bank should be able to provide you with any bank records that have been destroyed. Note that if your bank charges a fee for replacing bank records and providing any other service to help you to reconstruct records or provide information due to a disaster, you can claim a deduction in the income year that those fees are charged.

If you are unable to substantiate claims made in your tax returns or activity statements because your records have been lost or destroyed, it is generally the case that the ATO is still able to accept the claim without substantiation — for example, where it is not reasonably possible to obtain the original documents.

If you have a self-managed super fund (SMSF), it is a requirement to maintain compliance as an SMSF to keep certain records. If you have lost these records in a disaster, the ATO will consider a request for additional time to meet your reporting obligations (call 13 10 20). Where possible, the ATO should make available information that was previously reported for your SMSF.

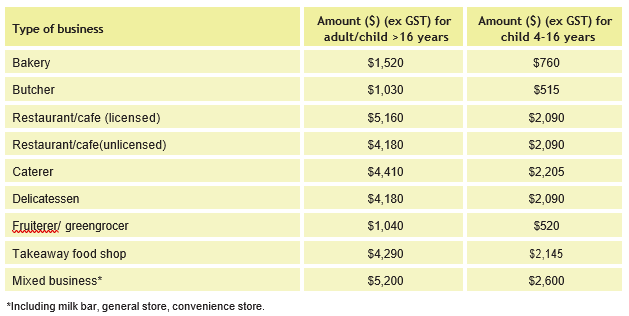

Taken goods for private use? Here’s the latest values

The ATO knows that many business owners naturally help themselves to their trading stock and use it for their own purposes. This common practice can occur in businesses such as butchers, bakers, corner stores, cafes and more.

Note that the ATO recognises that greater or lesser values may be appropriate in particular cases, and where you are able to provide evidence of a lower value, this should be used.

If you have any questions regarding this issue, please reach out to us for guidance

Two “main residences” is possible

The CGT exemption for a person’s home is only available in respect of one home owned at any given time. In other words, you can’t get two main residence exemptions applying to two different homes at the same time.

However, there is one exception to this rule – and that exception applies where a person has bought a new home before selling the old one. In this case, both homes can be entitled to the main residence exemption for an “overlap” period of up to six months.

But if the homeowner takes longer than six months to sell or dispose of the original home, a partial exemption will apply to one or other of the homes for the period in excess of six months. Generally, this will be the home that wasn’t the person’s main residence during this “excess period”.

However, a number of important conditions must be met in order to be able to use this concession in the first place – and this is where the guidance of your tax adviser is needed.

There is another important “overlapping” area in which the principles of not having two CGT-exempt main residences at the same time applies, and that is where “spouses” may have different main residences at the same time. Typically, this maybe where one spouse lives in their country or coastal home, while the other lives in their apartment in the city or interstate for work purposes (on a weekly or monthly basis, say).

But it also importantly includes the case where a couple start living together in a married or de-facto relationship, while one of the spouses retains their existing home and rents it (and therefore can apply a CGT concession to continue to treat it as their home).

Where this type of situation occurs there is a special rule that applies. The spouses must either: choose one of the homes to be the CGT-exempt main residence of both of them for this period; or each must choose the respective homes in which they live as their main residence – in which case generally they will each only get a half exemption on the home they choose for that overlap period.

Don’t ignore those tax debts: the ATO won’t!

Whilst the ATO went out of its way to assist businesses doing it tough during the COVID lockdowns, a more robust approach to collecting outstanding tax debts now seems to be the order of the day.

Other people’s money

A major part of the tax debts of many businesses represents the temporary withholding of other people’s money – employees’ PAYG withholding and their superannuation guarantee amounts. And the GST the business charges on the taxable supplies it makes doesn’t belong to the business either.

Some clients avoid mixing their own money and other people’s money. They have opened a separate BAS bank account for the withheld amounts so that those funds will be available when required, regardless of what happens in the business.

Director Penalty Notices

The ATO is particularly focused on employee entitlements and will not hesitate to issue Director Penalty Notices (DPNs) where there has been serious non-compliance by corporate entities.

Under a DPN, the sins of the company are visited on the directors, who will each be personally liable for any unpaid amounts.

As DPNs are a complex and serious matter, please contact us urgently should you receive one.

Disclosure to Credit Reporting Bureaus

One relatively recent development is the disclosure by the ATO of outstanding tax debts exceeding $100,000 to the various Credit Reporting Bureaus, which in turn could have an adverse impact on a business’ future ability to obtain finance. The ATO will contact the business ahead of making such a disclosure to give them an opportunity to set things right.

Simplified debt restructuring

Another relatively recent option, effective from 1 January 2021, is a less formal restructuring option for small incorporated businesses experiencing financial stress. Simplified debt restructuring is open to businesses with total debts of up to $1 million where the business has not undergone a restructure or a simplified liquidation in the last seven years. To be eligible, their current employee entitlement obligations and tax lodgements all have to be up to date.

The process involves appointing a small business restructuring practitioner (SBRP) and devising a plan setting out how much creditors would be paid under the plan if implemented. Creditors then vote on the plan, which is implemented if approved. The ATO is often

the major unsecured creditor in these matters, and we understand they have been quite open to approving many of the restructuring plans put forward.

The advantage of this method is that the directors continue to run the business throughout the restructuring process, subject to seeking the consent of the SBRP for any transactions falling outside the normal course of business.

In the meantime, there is a moratorium on the enforcement of debts by unsecured creditors and some secured creditors, while any personal guarantees given by a director or their spouse cannot be enforced except with leave from the court.

In order to qualify, a company has to be insolvent, or about to become insolvent. However, the core business has to be viable, or there would be little point in a restructure. This requires a realistic assessment of how the business is currently performing and what its future prospects are. If the core business is unviable due to industry changes, liquidation may be a more realistic option.

A number of small businesses have applied this option and successfully repaid debt on a compromised basis, emerging from an approved restructuring plan unburdened by unsustainable debt.

The taxation of super death benefits

Wondering if your beneficiaries will pay tax on your superannuation death benefits? The answer is it depends on a number of important factors.

Most people will have heard of Benjamin Franklin’s quote “in this world, nothing is certain except death and taxes”. He raises a valid point as the tax office will be ready to take their share of your death benefits when the time comes.

With that in mind, it is important to understand the tax rules that govern superannuation death benefits so you can ensure your benefits are distributed to your beneficiaries in the most tax- effective manner possible.

This article briefly summarises the three key factors that will determine whether your superannuation death benefits will be taxed when distributed to your beneficiaries.

1. Will a tax dependant receive the benefit?

The concept of super and tax law dependants was covered in detail in November’s Newsletter.

However, to recap, a tax dependant will not pay any tax on your super death benefits.

A tax dependant includes the following people:

1. A current spouse, including de facto and former spouse

2. Children under 18

3. A person who is financially dependent or in an interdependency relationship with the deceased.

TIP 1

The tax-free component of your superannuation benefit will always be received tax- free by your beneficiaries, regardless of whether they are a tax dependant or not.

TIP 2

If your superannuation death benefit is paid into your estate, your executor is responsible for deducting the appropriate tax when the amount is distributed to your beneficiaries. As your estate is not an individual, no Medicare Levy is payable which means non-tax dependants can avoid paying the additional 2% Medicare levy!

2. The underlying components of your benefit

Your current superannuation benefit may comprise of a taxable component and a tax- free component. As such, when you pass away, any death benefit payment made to your beneficiary(s) will reflect the proportions of the tax components of your member balance.

The taxable component of your superannuation benefit generally includes concessional contributions, such as superannuation guarantee and salary sacrifice contributions, and earnings made on your account balance.

However the taxable component of your superannuation benefit may also consist of an untaxed element if:

- Your benefit is paid from an untaxed fund (ie, your fund does not pay 15% tax on contributions or earnings – this is common in public sector funds and constitutionally protected funds, however

- most Australians are in taxed superannuation funds), or

- Your death benefit contains insurance proceeds and the fund has claimed a tax deduction for life insurance premiums

3. How will the death benefit be paid – lump sum or income stream?

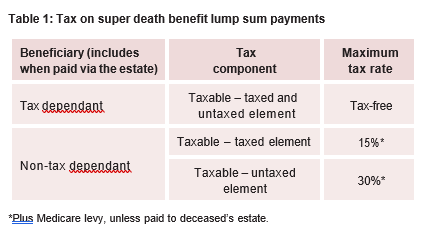

Lump sum death benefits

Lump sum superannuation death benefits paid to tax dependants directly or via your personal legal representative are not taxed.

However death benefits paid to non-tax dependants (ie, a financially independent adult child) are subject to tax on any taxable component of the lump sum superannuation benefit, which may include both a taxed and/or untaxed element.

Table 1 below summarises how the taxable component of a superannuation death benefit is taxed when it is paid as a lump sum in the event of a person’s death.

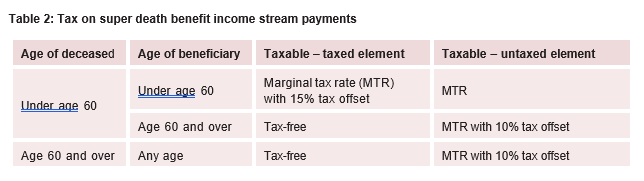

Death benefit income streams

Table 2 below summarises the tax payable on tax components based on the age of the beneficiary (at the date of payment) and the age of deceased (at the date of death).

As can be seen, the tax treatment depends on the age you pass away, the age of your beneficiary, as well as the underlying tax components of the income stream.

Need help?

The tax treatment of superannuation can be complex so please contact us if you need help or more information regarding your specific circumstances.