About This Newsletter

Welcome to the Collins House Private Wealth client information newsletter, your monthly tax and super update keeping you on top of the issues, news and changes you need to know. Should you require further information on any of the topics covered, please contact us via the details below.

T: 03 9629 6922

E: mail@collinshouse.com

Level 13, 90 Collins Street, Melbourne VIC 3000

PO Box 24175, Melbourne VIC 3000

Collins House Newsletter: October 2023

How to reduce your income tax bill using superannuation

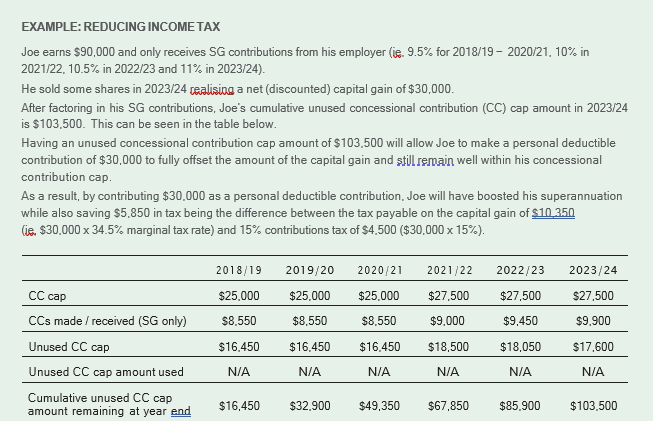

Did you know you can reduce your income tax by making a large personal tax-deductible contribution from your take-home pay to your super? This strategy may be particularly useful if you will be earning more income this financial year or if you have sold an asset this year and made a large capital gain.

What is a personal deductible contribution?

A personal deductible contribution is a type of concessional contribution that you make with your own money and claim as a personal tax deduction in your tax return, subject to meeting certain eligibility criteria (see Are you eligible to make a personal deductible contribution? on page 7).

Other types of concessional contributions include superannuation guarantee (SG) contributions from your employer and amounts you salary sacrifice to superannuation.

The cap on concessional contributions is currently $27,500 per year in 2023/24. However certain individuals may be eligible to use the “catch-up” concessional contribution rules to make a larger contribution.

What are catch-up concessional contributions?

You can carry forward any unused concessional contribution cap amounts that have accrued since 2018/19 for up to five financial years and use them to make concessional contributions in excess of the annual concessional contribution cap.

You can make a concessional contribution using the unused carry forward amounts provided your total superannuation balance at the end of the previous financial year (ie, 30 June 2023) is below $500,000.

Once you start to use some of your unused cap amounts, the rules operate on a first-in first-out basis. That is, any unused cap amounts are applied to increase your concessional contribution cap in order from the earliest year to the most recent year. So, when you use some of your unused cap from prior years (by making additional superannuation contributions), the unused cap from the earliest of the five-year period is used first.

And remember, if you don’t use your accrued carry forward amounts after five years, your unused cap amounts will expire. So it’s best to use it before you lose it!

Carry forward contributions may provide strategic opportunities to make larger personal deductible contributions in financial years where you may have a higher level of taxable income, for example, due to assessable capital gains. See the example below.

Seek advice It’s important to seek advice before you make any superannuation contribution. Getting it wrong could mean a loss of all or part of your deduction and may also cause you to exceed the contribution caps which can lead to paying excess contributions tax.

Changes to unfair contract terms laws

What businesses need to know

Soon to be implemented changes to the Australian Consumer Law will provide additional protection to consumers and small businesses prohibiting the proposal, use or reliance on unfair contract terms in standard form contracts

The ACCC recognises that:

“… standard form contracts provide a cost- effective way for many businesses to contract with significant volumes of consumer or small business customers. However, these contracts are largely imposed on a ‘take it or leave it’ basis and are usually drafted to the advantage of the party offering them.”

Currently under the laws protecting consumers and small businesses from unfair terms in standard for contracts, where particular terms of a contract are found to be unfair, a Court can only declare those terms void. This provides little motivation to ensure the terms of standard form contracts are, in fact, fair.

From 9 November 2023, in addition to expanding the coverage of the unfair contract term laws to a wider range of small businesses, Courts will now be able

to impose substantial penalties where unfair terms have been included in a standard form contract, and a party to the contract is a small business (that is, small businesses with an annual turnover of less than $10m or fewer than 100 employees).

With the maximum penalties increasing to $2.5m for individuals, and for businesses to the greater of $50 million or three times the value of the “reasonably attributable” benefit obtained from the conduct, the ACCC is encouraging businesses to review their standard form contracts prior to these changes taking effect.

You can view more information about changes to the unfair contract terms laws on the ACCC’s website here and here.

In Makrylos v FCT [2023] FCA 971, land acquired by a property developer was treated as trading stock from the date of its original acquisition, and not a later date proposed by the taxpayer. This meant, among other things, that his profit was calculated on the original purchase price of the land and not the later (and larger) market value at the time it had been “ventured” into the relevant property development activity, as claimed by the taxpayer. It also had an influence on what costs he could claim as a deduction and when he could claim them.

The Federal Court came to its decision notwithstanding that the taxpayer lived on the property at various times. However, the taxpayer was also an experienced property developer who subdivided the land, albeit this was not required for the construction of a family home and caretaker’s residence, which is what the taxpayer claimed was his original intention for the land.

The fact that the taxpayer periodically lived in the dwelling on the land but left it vacant for significant periods did not assist him as the Court found that his intention from the time when he purchased it was to treat it as trading stock of his business.

The Federal Court said that it would have come to the same result even if he was not a property developer, but had “merely” acquired it for profit- making purposes in a one-off transaction.

So, if you buy property for a property development purpose for which documentary evidence exists, it may not matter if you rent it and/or live in it first, especially if you are a property developer.

And one thing for sure, it won’t help if you staked out the property for subdivision purposes soon after you acquire it!

Small business skills and training boost

Looking to boost your employees’ skills and your tax deductions at the same time? Then keep reading to see if you could be eligible for the small business skills and training boost!

If you run a small or medium business and are planning on investing in, or recently invested in, training your employees, taking care to ensure the training is provided by a registered training provider could mean you can claim an additional 20% bonus tax deduction at tax time.

Which training expenses are eligible for the bonus?

Eligible expenditure must be:

- for training your employees, in-person in Australia, or online

- for training provided by registered training providers (for example see training.gov.au and National Register of Higher Education Providers)

- charged by the registered training provider for course fees and related items such as books and equipment (for deductions claimed over time such as depreciation, the bonus deduction will be calculated as 20% of the full amount and claimed upfront)

- incurred between 29 March 2022 and 30 June 2023 (the bonus is claimed in your 2022-23 tax return) or between 1 July 2023 and 30 June 2024 (the bonus is claimed in your 2023-24 tax return).

Which training expenses are not eligible for the bonus?

- Training you provide to your employees yourself (eg on-the-job training)

- Training for yourself if you are self-employed or in a partnership

- Training provided to independent contractors

- Training provided by non-registered providers

- Training provided by registered providers that are associates of yours

- Expenses not charged by the registered training provider eg if an intermediary has charged a commission on top of the training course.

To avoid a costly unexpected FBT liability come 31 March, make sure the training relates to an employee’s current duties or helps them get a promotion or pay-rise in their current role – see our September 2023 Newsletter. (Paying an employee’s HECs or other study-loan repayment will usually attract FBT.) If you are uncertain whether your training expenditure is deductible, eligible for the bonus, or concerned it may attract FBT, reach out to us – we’d love to help.

Don’t overlook the CGT small business roll-over concession

The CGT small business concessions are invaluable to those who make a capital gain from a small business. They can eliminate a gain entirely; they can reduce a gain; and they can allow for the gain to be CGT-free if paid into a superannuation fund.

But it is often forgotten that the gain can also be rolled over.

And this concession can be very useful depending on your circumstances and business intentions, especially where it may be used in conjunction with the other CGT small business concessions.

Broadly, this roll-over concession allows you to roll-over a capital gain if a “replacement asset” is acquired within the 2-year “replacement asset period”.

However, the rolled over gain will be reinstated if the amount of the capital gain is not expended on acquiring a replacement asset within this time period. In this way, the roll-over offers a 2-year deferral of the assessment and taxation of the capital gain.

But apart from the advantage of the 2-year deferral (which will also give you time to think about what to do with the money and whether to go back into business), the reinstated gain is eligible for the retirement concession – which allows you to take a capital gain of up to $500,000 tax-free if you are 55 or over, or otherwise requires you to pay the gain into your super fund. Moreover, the 2-year deferral may allow you to access this concession in the most advantageous way – namely, when you are aged 55 years or over!

Likewise, a capital gain will be reinstated if a replacement asset is acquired, but after the 2-year period, it ceases to be used as a business asset (eg it is sold or taken for private use).

In this case the reinstated gain is also entitled to the retirement concession. But additionally it is also entitled to be rolled over again, which can be invaluable to a small business owner in a range of circumstances (even to the extent of continually rolling over the gain until retirement).

For example, say you make a capital gain from selling your gym business. This capital gain can be rolled over by acquiring new equipment in other gyms you own. And each time these wear out and are disposed of, the capital gain reinstated can be used to acquire replacement equipment. This can be done continuously until you reach retirement and then finally crystalise the reinstated gain. Of course, like all areas of tax, it is an area which requires the considered advice of a taxation professional – especially in relation to any tax planning opportunities!

Are you eligible to make a personal deductible contribution?

Personal deductible contributions can allow individuals to claim a tax deduction for contributions they have made to superannuation provided they meet certain requirements. So what are these requirements and what should you look out for?

Eligibility requirements

You will be eligible to claim a deduction for your personal superannuation contributions if:

- You meet the aged based rules

- Your taxable income is more than the amount you want to claim as a deduction (ie your deduction can’t give you a tax loss)

- You make the contribution to a complying superannuation fund

- You give a special notice to your fund telling the trustee how much you want to claim

- You give your fund that notice within strict timeframes

- Your fund sends you an acknowledgement confirming your notice has been received and is valid.

You must meet all of the above criteria otherwise you won’t be eligible to claim a deduction for your contributions.

Meeting the age-based rules

If you are between age 18 and 66 when you make your contribution, there are no age-based rules for you to meet. This means there are no age restrictions in order to make a deductible contribution.

If you are aged 67 to 74 when you make your contribution, you can only claim a deduction if you meet the “work test” or the “work test exemption” in that year.

To meet the work test, you need to work for at least 40 hours in a 30-day consecutive period during the financial year and be paid for that work.

Alternatively, the work test exemption can be used if you satisfy all of the following rules:

- You are aged between 67 to 74

- You satisfied the work test in the previous financial year

- Your total superannuation balance was below $300,000 the previous 30 June (ie 30 June 2023)

- You have not made use of the work test exemption in a previous financial year (ie it can only be used once).

If you are aged 75 or older at the time you make your contribution, you can only claim a deduction if your contribution was made before the 28th day of the month after your 75th birthday and you met the work test above. For example, if you turn 75 in September 2023, your contribution must be

superannuation fund by 28 October 2023. This is a special rule that applies around an individual’s 75th birthday.

Unfortunately, once a person reaches age 75, you can no longer make any deductible superannuation contributions. The only contributions that can be made are

downsizer contributions, superannuation guarantee contributions

or contributions your employer is obliged to make for you under an award.

Timeframes to adhere to

You must give your fund the notice form before the earlier of:

- The day you lodge your personal income tax return for the year in which you made your contribution, or

- 30 June of the following year.

However, certain events may occur which mean you must submit your notice and receive acknowledgement from your fund prior to the above timeframes. For example, you must submit and receive acknowledgement from your fund prior to:

- Withdrawing any funds

- Rolling over to another fund

- Splitting contributions with your spouse, or

- Commencing a pension.

If you do not give your notice to your fund before these events occur, you will lose some or all of the deduction amount.

What happens next?

Once you have told your fund that you want to claim a deduction for your personal contribution, it will count towards your concessional contributions cap. Your fund will then deduct contributions tax of 15% from your contribution.

If you change your mind and no longer want to claim the entire amount as a tax deduction, you can vary your notice to reduce the amount you are claiming, provided you are still within the timeframes mentioned above.

It is also important to claim the deduction in your personal income tax return for the year the contribution was made. If you forget to claim the deduction, your contribution will count towards your non-concessional contributions cap and could cause you to exceed that cap. As you can see, the contribution rules are complex so if you’re thinking about making a personal deductible contribution and not sure if you meet the eligibility requirements, contact us today for a chat.